The Carry Trade Explained: Earning the Rate Differential

The carry trade is one of the oldest ways to make money in FX, and one of the fastest to blow up. Here is how it works, where the return comes from, and what kills it.

The carry trade is one of the oldest ideas in currency markets. Borrow where money is cheap, park it where money pays more, and pocket the difference. For long stretches it works quietly and reliably. Then, every few years, it comes apart in a matter of days and takes a lot of people with it. Understanding both halves of that story is the whole point of this piece.

What the carry trade actually is

At its simplest, a carry trade means holding a higher-yielding currency and funding it with a lower-yielding one. If one currency pays 5% and another pays 1%, a trader who is long the first against the second collects roughly the 4% gap for as long as the position is held. In the futures and spot market this shows up as the rollover or swap you earn or pay for holding a position overnight.

The currency you borrow is the funding currency. Historically the yen and the Swiss franc have played that role because their rates sat low for years, and the dollar takes the role whenever US rates are at the bottom of the cycle. The currency you hold is the higher-yielder, often a higher-rate G10 name or an emerging-market currency.

Where the return comes from

A carry trade has two possible sources of return, and it helps to keep them separate.

The first is the interest differential itself, the yield you collect simply for holding the position. This is the steady, mechanical part. It accrues a little at a time, day after day, as long as the rate gap stays in your favour.

The second is any move in the exchange rate. If the higher-yielder also appreciates while you hold it, that capital gain sits on top of the yield. This is where carry and the broader rate-differential story overlap, because a widening expected differential tends to pull the higher-yielder up as well as pay you to hold it. I wrote about that mechanism in detail in rate differentials explained.

The trouble is that the second source can turn negative fast, and when it does, it dwarfs the yield.

Why it works most of the time

In a calm market, capital hunts for yield. When volatility is low and trends are stable, money flows steadily toward the currencies that pay more, which supports those currencies and rewards everyone already holding them. The trade becomes self-reinforcing for a while. Low volatility is the essential ingredient. As long as nothing frightens the market, the carry grinds higher and the yield keeps landing.

This is why carry trades tend to perform best in quiet, trending, risk-friendly conditions, and why they are so closely tied to the market’s appetite for risk.

What kills it

Carry has been described as picking up pennies in front of a steamroller, and the description is fair. The yield you collect is small and steady. The loss when it unwinds is large and sudden.

The steamroller is a spike in volatility, almost always driven by a shift into risk-off. When fear enters the market, the mechanics reverse violently. Traders who borrowed the funding currency have to buy it back to close out, all at once, which sends the funder sharply higher and the higher-yielder sharply lower. Because so many people hold the same crowded carry positions, the exit is a stampede through a narrow door. Years of accumulated yield can vanish in a single session.

That is the honest risk. Carry does not fail gently. It fails all at once, and it fails exactly when the wider market is already under stress. I cover the mechanics of that regime shift in risk-on, risk-off.

How I think about it

I treat carry as a strategy that is only attractive when several things line up at once, and I am wary of it the moment they stop lining up.

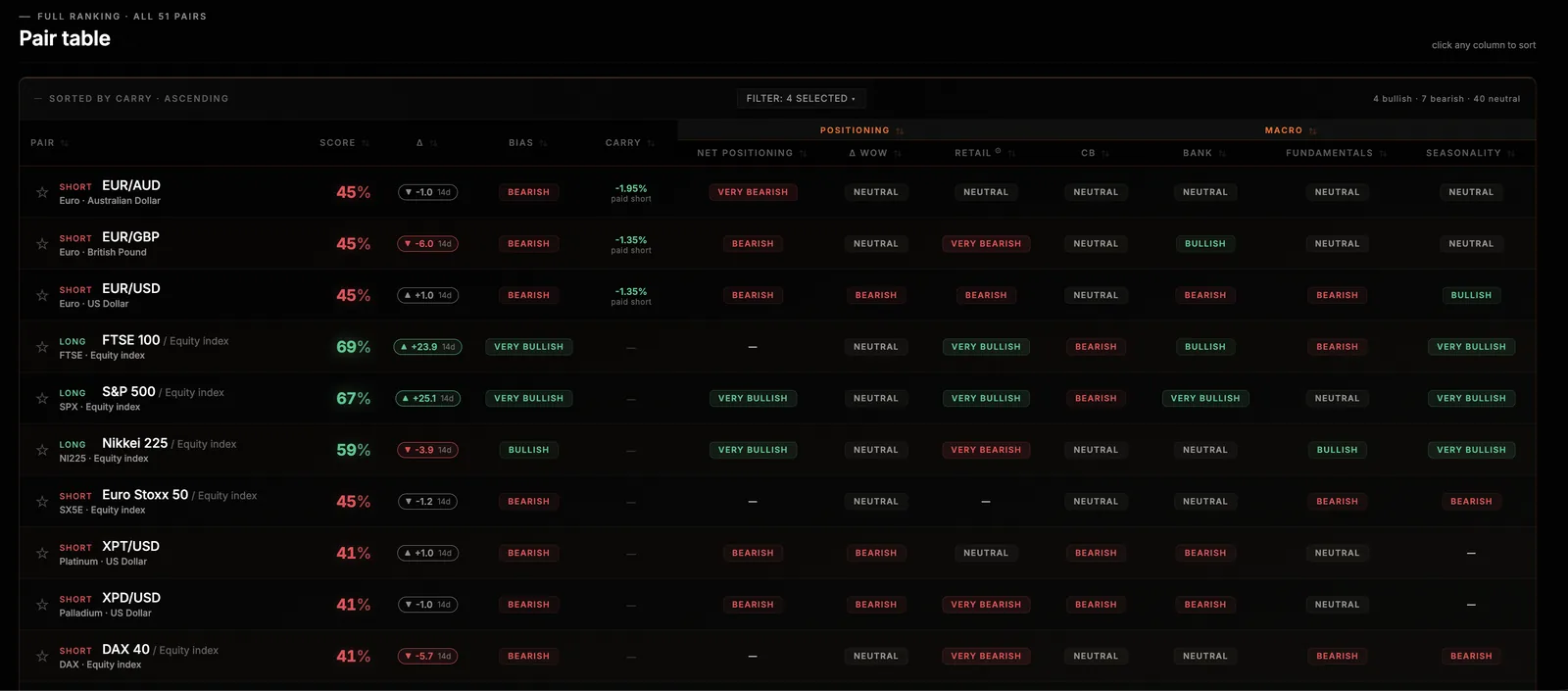

I want the rate differential to be genuinely wide, and ideally still widening rather than about to narrow. I want the volatility environment to be calm, because carry and rising volatility do not coexist for long. I want the broader risk backdrop to be supportive rather than fragile. And I pay attention to positioning, because a carry trade that the entire speculative crowd already holds is the one most exposed to a violent unwind. That is exactly the kind of crowded extreme I look for in the COT report.

When the differential is wide, volatility is low, the risk mood is constructive and positioning is not yet stretched, carry is doing what it is supposed to do. When volatility starts to lift and the crowd is already all-in, the yield stops being worth the risk, and that is the point to respect the steamroller.

In WatchTower Terminal I keep the rate differentials, the macro backdrop and the positioning for each pair in one view, so I can see whether the conditions that make carry work are actually in place, rather than reaching for the yield and hoping the calm holds.

The carry trade is a good servant and a dangerous master. The yield is real, and so is the tail risk. Knowing which environment you are in is most of the job.

Read the market the way this page describes.

WatchTower Terminal turns bank research, positioning and central-bank data into one clear read across FX, metals and global indices. Start free, no card required.